Page 134 - BKT Annual Report 2023 EN

P. 134

65 BANKA KOMBËTARE TREGTARE

Notes to the Consolidated Financial Statements for the year ended 31 December 2023

(amounts in USD, unless otherwise stated)

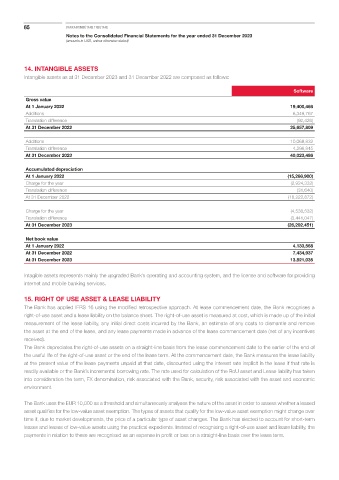

14. INTANGIBLE ASSETS

Intangible assets as at 31 December 2023 and 31 December 2022 are composed as follows:

Software

Gross value

At 1 January 2022 19,400,468

Additions 6,349,767

Translation difference (92,426)

At 31 December 2022 25,657,809

Additions 10,068,832

Translation difference 4,296,845

At 31 December 2023 40,023,486

Accumulated depreciation

At 1 January 2022 (15,266,900)

Charge for the year (2,924,332)

Translation difference (31,640)

At 31 December 2022 (18,222,872)

Charge for the year (4,538,532)

Translation difference (3,441,047)

At 31 December 2023 (26,202,451)

Net book value

At 1 January 2022 4,133,568

At 31 December 2022 7,434,937

At 31 December 2023 13,821,035

Intagible assets represents mainly the upgraded Bank’s operating and accounting system, and the license and software for providing

internet and mobile banking services.

15. RIGHT OF USE ASSET & LEASE LIABILITY

The Bank has applied IFRS 16 using the modified retrospective approach. At lease commencement date, the Bank recognises a

right-of-use asset and a lease liability on the balance sheet. The right-of-use asset is measured at cost, which is made up of the initial

measurement of the lease liability, any initial direct costs incurred by the Bank, an estimate of any costs to dismantle and remove

the asset at the end of the lease, and any lease payments made in advance of the lease commencement date (net of any incentives

received).

The Bank depreciates the right-of-use assets on a straight-line basis from the lease commencement date to the earlier of the end of

the useful life of the right-of-use asset or the end of the lease term. At the commencement date, the Bank measures the lease liability

at the present value of the lease payments unpaid at that date, discounted using the interest rate implicit in the lease if that rate is

readily available or the Bank’s incremental borrowing rate. The rate used for calculation of the RoU asset and Lease liability has taken

into consideration the term, FX denomination, risk associated with the Bank, security, risk associated with the asset and economic

environment.

The Bank uses the EUR 10,000 as a threshold and simultaneously analyses the nature of the asset in order to assess whether a leased

asset qualifies for the low-value asset exemption. The types of assets that qualify for the low-value asset exemption might change over

time if, due to market developments, the price of a particular type of asset changes. The Bank has elected to account for short-term

leases and leases of low-value assets using the practical expedients. Instead of recognising a right-of-use asset and lease liability, the

payments in relation to these are recognised as an expense in profit or loss on a straight-line basis over the lease term.