Page 119 - BKT Annual Report 2023 EN

P. 119

ANNUAL REPORT 2023 50

Notes to the Consolidated Financial Statements for the year ended 31 December 2023

(amounts in USD, unless otherwise stated)

v. Concentrations of credit risk

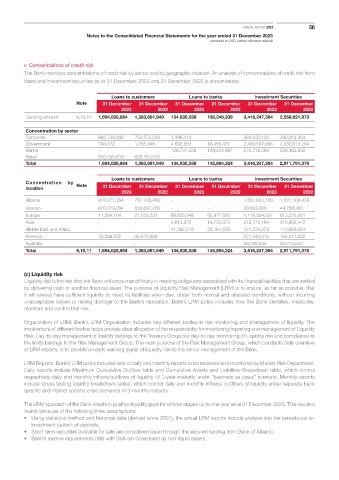

The Bank monitors concentrations of credit risk by sector and by geographic location. An analysis of concentrations of credit risk from

loans and investment securities as at 31 December 2023 and 31 December 2022 is shown below:

Loans to customers Loans to banks Investment Securities

Note 31 December 31 December 31 December 31 December 31 December 31 December

2023 2022 2023 2022 2023 2022

Carrying amount 9,10,11 1,694,028,984 1,383,681,949 134,830,538 138,246,339 3,416,247,364 2,558,621,973

Concentration by sector

Corporate 882,738,293 753,572,033 3,396,419 - 360,933,122 342,014,464

Government 794,872 1,355,346 4,692,563 16,465,437 2,480,597,956 2,030,613,264

Banks - - 126,741,556 129,428,887 574,716,286 539,163,650

Retail 810,495,819 628,754,570 - - - -

Total 1,694,028,984 1,383,681,949 134,830,538 145,894,324 3,416,247,364 2,911,791,378

Loans to customers Loans to banks Investment Securities

Concentration Note

by location 31 December 31 December 31 December 31 December 31 December 31 December

2023 2022 2023 2022 2023 2022

Albania 978,277,354 767,785,462 - - 1,661,623,750 1,527,106,476

Kosovo 670,879,294 558,697,265 - - 39,803,280 44,769,360

Europe 11,584,104 21,525,333 89,655,048 92,977,620 1,119,504,537 813,078,001

Asia - - 3,613,272 19,755,072 219,772,164 218,982,412

Middle East and Africa - - 41,562,218 33,161,632 124,531,273 113,629,254

America 33,288,232 35,673,889 221,243,815 165,011,032

Australia - - - - 29,768,545 29,214,843

Total 9,10,11 1,694,028,984 1,383,681,949 134,830,538 145,894,324 3,416,247,364 2,911,791,378

(c) Liquidity risk

Liquidity risk is the risk that the Bank will encounter difficulty in meeting obligations associated with its financial liabilities that are settled

by delivering cash or another financial asset. The purpose of Liquidity Risk Management (LRM) is to ensure, as far as possible, that

it will always have sufficient liquidity to meet its liabilities when due, under both normal and stressed conditions, without incurring

unacceptable losses or risking damage to the Bank’s reputation. Bank’s LRM policy includes how the Bank identifies, measures,

monitors and control that risk.

Organization of LRM: Bank’s LRM Organization includes two different bodies in the monitoring and management of liquidity. The

involvement of different bodies helps provide clear allocation of the responsibility for monitoring/reporting and management of Liquidity

Risk. Day-to-day management of liquidity belongs to the Treasury Group but day-to-day monitoring of Liquidity risk and compliance to

the limits belongs to the Risk Management Group. The main purpose of the Risk Management Group, which conducts daily overview

of LRM reports, is to provide an early warning signal of liquidity risk to the senior management of the Bank.

LRM Reports: Bank’s LRM policy includes sets of daily and monthly reports to be reviewed and monitored by Market Risk Department.

Daily reports include Maximum Cumulative Outflow table and Cumulative Assets and Liabilities Breakdown table, which control

respectively daily and monthly inflows/outflows of liquidity till 1-year maturity under “business as usual” scenario. Monthly reports

include stress testing liquidity breakdown tables, which control daily and monthly inflows/ outflows of liquidity under separate bank

specific and market specific crisis scenarios till 3-months maturity.

The LRM approach of the Bank results in positive liquidity gaps for all time stages up to one year as at 31 December 2023. This resulted

mainly because of the following three assumptions:

• Using statistical method and historical data (derived since 2001), the actual LRM reports include analysis into the behavioural re-

investment pattern of deposits;

• Short term securities available for sale are considered liquid through the secured funding from Bank of Albania;

• Bank’s reserve requirements held with BoA are considered as non-liquid assets.